Wed, Apr 8, 2026

Global Edition

Understanding VWAP: A Trader's Essential Tool for Futures Trading

2026-04-08

In the world of futures trading, navigating market volatility can be daunting, especially for beginners. One tool that has gained traction among traders is the Volume Weighted Average Price (VWAP). Understanding VWAP is essential for making informed trading decisions, as it offers insights into price momentum and market sentiment, which can significantly enhance your trading strategy.

What is VWAP?

VWAP stands for Volume Weighted Average Price. It is a technical indicator that helps traders assess the average price a security has traded at throughout the day, weighted by volume. The calculation takes every trade's price and weighting it by the number of shares traded at that price. This contrasts with a simple average price, providing a more accurate reflection of the market's activity across different price levels.

The formula for calculating VWAP is:

VWAP = (Cumulative (Price * Volume)) / Cumulative VolumeBy using VWAP, traders can gauge the general direction of the market. A price above the VWAP suggests bullish sentiment, while a price below indicates bearish sentiment.

Why is VWAP Important?

VWAP serves multiple purposes in trading. It acts as a trading benchmark and liquidity measure, providing a comprehensive view of price action throughout the trading session. This makes it especially valuable for institutional traders who need to execute large orders without heavily impacting the market.

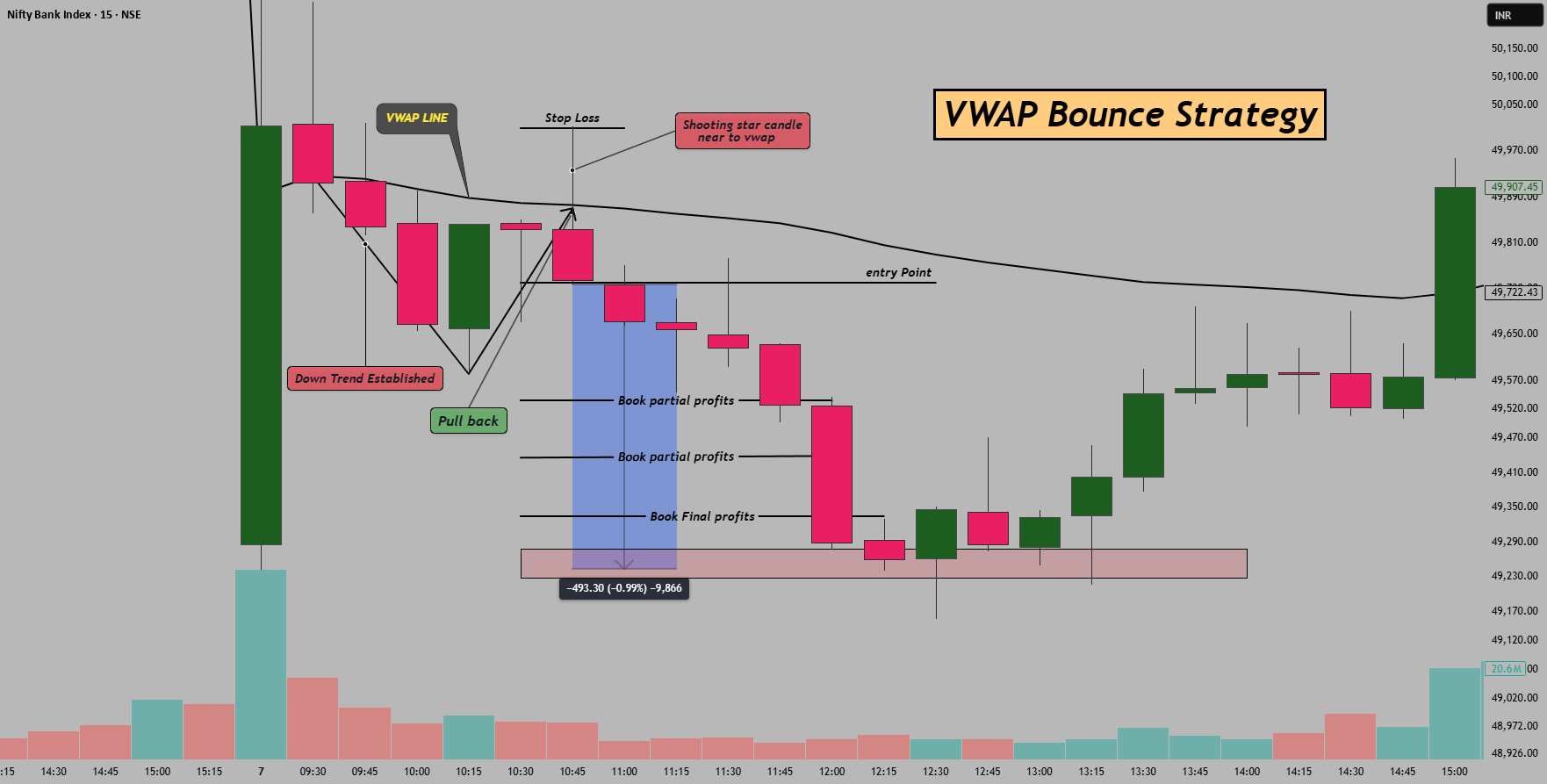

Moreover, VWAP can signal potential entry and exit points. For instance, if a trader observes a breakout above the VWAP, it may indicate a good buying opportunity. Conversely, if the price dips below the VWAP, it might suggest selling pressure. Understanding this dynamic can be crucial in setting up informed trading strategies.

Practical Examples of VWAP Usage

To illustrate how VWAP can be applied in trading scenarios, let’s consider two hypothetical futures trades.

1. Bullish Trade Setup: A trader notices that the price of a futures contract has moved above the VWAP after a period of consolidation. This breakout above the VWAP coupled with increasing trading volume may lead the trader to enter a long position, anticipating further price appreciation. The trader might set a stop-loss just below the VWAP to protect against sudden reversals.

2. Bearish Trade Setup: Conversely, if the price drops below the VWAP and starts to show strong selling momentum, the same trader could view this as a signal to enter a short position. Again, a stop-loss might be placed above the VWAP to minimize potential losses.

Such examples demonstrate how VWAP can serve as a guidepost, offering traders clarity on when to enter or exit positions based on real-time market dynamics.

Common Mistakes to Avoid

While VWAP can provide valuable insights, traders should be wary of some common pitfalls. One common mistake is using VWAP in isolation without considering other indicators. Relying solely on VWAP may lead to false signals; thus, integrating VWAP with other tools, such as moving averages or RSI, can enhance its effectiveness.

Another mistake is overreacting to short-term fluctuations. Since VWAP is calculated based on cumulative volume throughout the trading day, it is subject to intraday noise. Quick price movements may deviate from the VWAP temporarily, misleading traders into making premature decisions.

Lastly, new traders often struggle with timeframes. VWAP is typically recalibrated daily, meaning traders need to apply it in the correct context. Misinterpreting the VWAP for longer-term strategies can also lead to inappropriate trading decisions.

VWAP vs. Moving Averages

When comparing VWAP to moving averages, it's worth noting that both are used for different market analysis purposes. VWAP provides a volume-weighted perspective, making it excellent for day trading and intraday strategies. In contrast, moving averages, such as the 50-day or 200-day averages, provide a broader trend perspective over a more extended period. Here's a quick comparison:

FeatureVWAPMoving AveragesCalculationVolume weightedSimple or exponentialPrimary UseDay tradingLong-term trend analysisResponsivenessHighly reactive to close priceSmoother responses to noiseRecalibration FrequencyDailyDepends on period (e.g., daily, weekly)

This nuance is crucial for traders when choosing which tool to utilize based on their trading goals and styles.

Next Steps for Utilizing VWAP

For traders looking to incorporate VWAP into their strategies, here are some actionable steps:

1. Learn the Calculation: Familiarize yourself with the formula and how VWAP is derived. Many trading platforms calculate VWAP automatically, but understanding the underlying math can enhance your trading acumen.

2. Backtest Strategies: Implement VWAP in your trading strategy and backtest it in a simulation or paper trading environment. This allows you to see how VWAP would have performed historically under various market conditions.

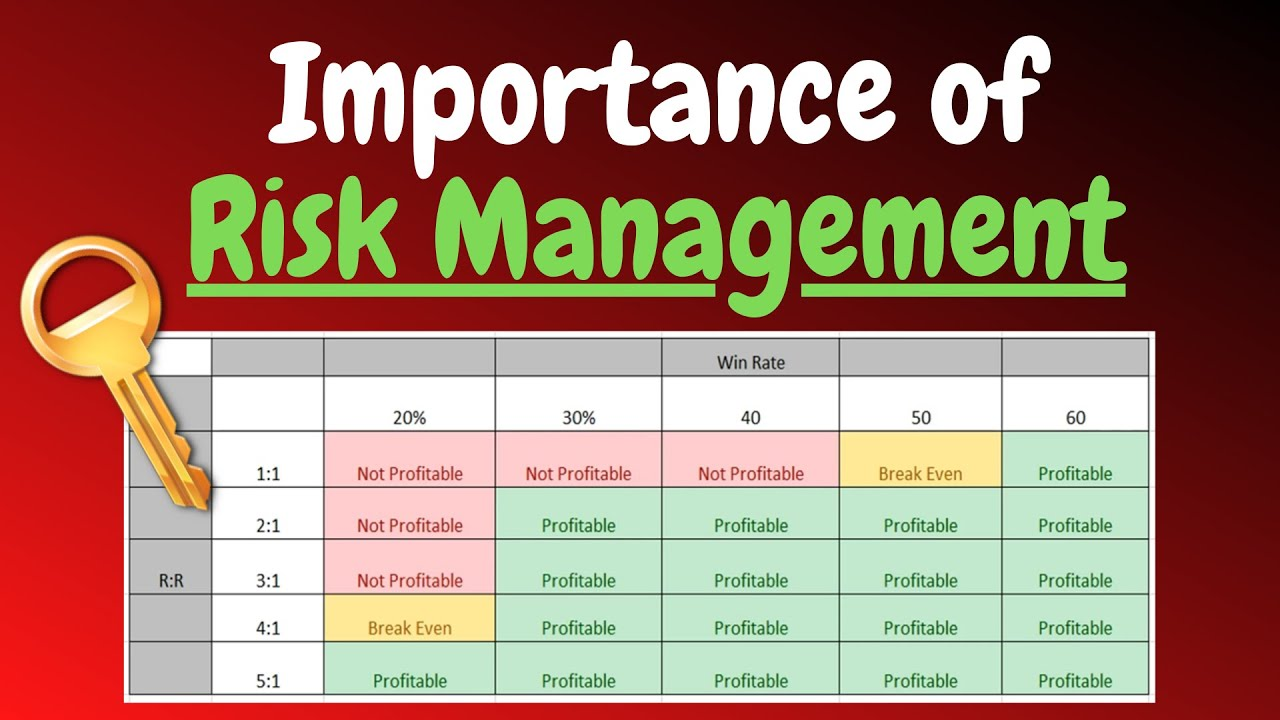

3. Integrate with Risk Management: Always couple your VWAP strategies with robust risk management plans, such as setting stop-loss orders and determining position sizes based on your overall trading capital.

By adopting these steps and remaining mindful of potential missteps, traders can leverage VWAP effectively to improve decision-making and market insight.

Conclusion

VWAP is more than just a technical indicator; it is a vital trading tool that can enhance any futures trader's toolkit. By understanding what VWAP represents, how to use it in various scenarios, and the common pitfalls to avoid, traders can position themselves for more informed and strategic trading decisions. Grounded in its real-time relevance, VWAP provides a comparative advantage in navigating the complexities of today's futures markets.

Learn about Volume Weighted Average Price (VWAP), a key trading indicator used by futures traders. This guide breaks down its significance, practical applications, and common pitfalls, ensuring you leverage VWAP effectively in your trading strategy.

Other Posts

Understanding Backtesting: Its Relevance and Future Outlook in Trading

Apr 8, 2026

Understanding Risk Management in Trading: A Beginner's Guide

Apr 8, 2026

Beginner's Guide to Trading Strategies: 00:00 Key Open Explained

Apr 8, 2026

Apex Trader Funding vs FTMO: Which Prop Firm Is Right for You?

Apr 8, 2026

Understanding Google AdSense Rejections: Causes, Solutions, and Prevention Tips

Apr 8, 2026

Exporting Tick Data from NinjaTrader 8: NinjaScript Guide for Traders

Apr 8, 2026